When a missing Will emerged after an estate had been settled

Lenders

D-Risk

Climate change business impact assessment for a UK lender

A UK lender needed a clearer view of how climate change could affect the flood risk profile of its commercial mortgage portfolio. D-Risk delivered a two-tier assessment that helped the lender understand portfolio exposure, identify high-risk assets and explore practical mitigation options to protect long-term value.

Requirements

Following the introduction of the Prudential Regulation Authority’s SS3/19 guidance, the lender required a detailed review of climate-related risk across its commercial mortgage back book. The first priority was to assess the existing flood risk profile of the portfolio and understand how that risk could change over time as a result of climate change. A second, more detailed tier of analysis was then needed for the highest-risk properties, with a focus on potential business continuity issues and measures that could reduce future exposure.

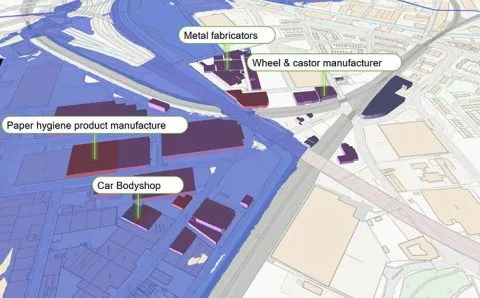

Our Solution

D-Risk combined its specialist expertise with the support of industry-leading partners to provide an overview of the lender’s climate risk profile across the full lifecycle of its existing mortgages. Using defined search parameters and geospatial analysis, the team was able to separate lower-risk assets from those requiring further review. For properties falling outside the lender’s acceptable risk threshold, D-Risk carried out deeper analysis and presented tailored mitigation options designed to help protect future asset value and operational resilience.

The Results

The lender gained a coherent view of how climate change could affect the future risk profile of its commercial mortgage portfolio. This provided greater confidence in the value and resilience of the assets it held, while also helping to shape future lending decisions. The outcome enabled the lender to adopt more robust risk management principles, reduce the potential for losses in value and identify customers who may require additional support in response to future climate-related risks.

Two-tier assessment

Portfolio-wide analysis followed by deeper review of the highest-risk assets

Climate risk visibility

Improved understanding of future flood exposure across the commercial mortgage book

Actionable mitigation

Tailored options to support business continuity and protect asset value

Get in touch

More Case Studies